All Categories

Featured

Table of Contents

The are entire life insurance and universal life insurance coverage. The money worth is not added to the death benefit.

After 10 years, the money worth has actually grown to about $150,000. He takes out a tax-free lending of $50,000 to begin a service with his sibling. The plan lending rates of interest is 6%. He pays off the funding over the next 5 years. Going this course, the rate of interest he pays returns into his plan's money worth rather than a banks.

Infinite Banker

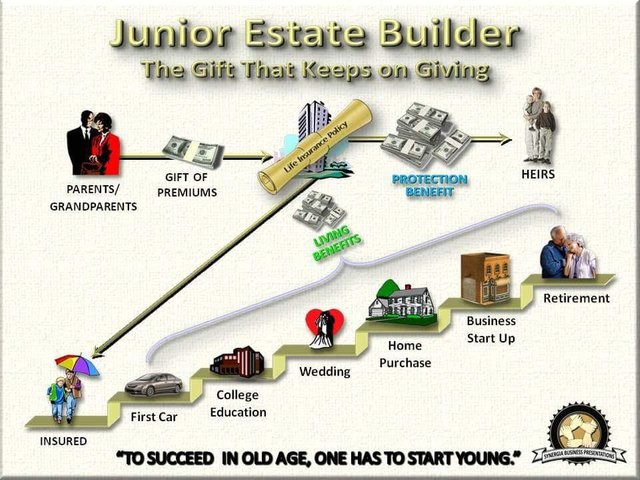

The principle of Infinite Banking was developed by Nelson Nash in the 1980s. Nash was a money expert and follower of the Austrian institution of economics, which promotes that the value of goods aren't explicitly the result of typical financial frameworks like supply and need. Rather, people value cash and items in different ways based upon their financial standing and needs.

One of the pitfalls of standard financial, according to Nash, was high-interest prices on fundings. Long as banks set the rate of interest prices and funding terms, people didn't have control over their own wealth.

Infinite Financial needs you to own your monetary future. For ambitious people, it can be the finest monetary tool ever. Below are the advantages of Infinite Financial: Perhaps the single most helpful facet of Infinite Banking is that it enhances your money circulation.

Dividend-paying whole life insurance is really reduced danger and provides you, the insurance holder, an excellent bargain of control. The control that Infinite Banking uses can best be organized right into 2 categories: tax obligation benefits and asset defenses.

Youtube Infinite Banking

When you make use of whole life insurance policy for Infinite Financial, you get in right into an exclusive agreement between you and your insurance policy business. These securities may differ from state to state, they can consist of protection from property searches and seizures, defense from judgements and protection from creditors.

Whole life insurance policies are non-correlated properties. This is why they work so well as the monetary structure of Infinite Financial. No matter what takes place in the market (supply, property, or otherwise), your insurance plan retains its well worth. Also numerous people are missing out on this vital volatility buffer that assists protect and expand riches, instead splitting their money right into 2 containers: bank accounts and financial investments.

Market-based financial investments grow riches much faster however are subjected to market variations, making them naturally dangerous. Suppose there were a 3rd container that offered safety and security yet likewise modest, surefire returns? Whole life insurance policy is that 3rd pail. Not just is the rate of return on your whole life insurance plan ensured, your survivor benefit and premiums are additionally ensured.

This framework lines up flawlessly with the principles of the Continuous Wide Range Approach. Infinite Financial attract those looking for better financial control. Below are its major benefits: Liquidity and availability: Plan financings provide instant accessibility to funds without the constraints of traditional financial institution car loans. Tax obligation performance: The money value expands tax-deferred, and policy financings are tax-free, making it a tax-efficient tool for constructing wide range.

Infinite Banking Book

Possession protection: In lots of states, the cash value of life insurance policy is secured from creditors, adding an additional layer of financial safety. While Infinite Banking has its qualities, it isn't a one-size-fits-all solution, and it features significant disadvantages. Right here's why it may not be the most effective strategy: Infinite Financial typically requires elaborate policy structuring, which can puzzle insurance holders.

Imagine never ever having to stress over small business loan or high rate of interest rates once again. What if you could borrow money on your terms and construct wealth at the same time? That's the power of limitless banking life insurance policy. By leveraging the money value of whole life insurance policy IUL policies, you can grow your riches and obtain money without depending on traditional banks.

There's no set lending term, and you have the liberty to pick the repayment timetable, which can be as leisurely as repaying the finance at the time of death. This adaptability encompasses the servicing of the finances, where you can choose for interest-only payments, maintaining the finance equilibrium flat and convenient.

Holding money in an IUL dealt with account being attributed rate of interest can often be far better than holding the cash money on down payment at a bank.: You have actually always desired for opening your own pastry shop. You can borrow from your IUL policy to cover the preliminary expenditures of renting out an area, purchasing tools, and hiring staff.

How To Create Your Own Bank

Individual lendings can be gotten from standard financial institutions and debt unions. Borrowing money on a debt card is generally really costly with annual percent prices of passion (APR) often getting to 20% to 30% or more a year.

The tax treatment of plan fundings can vary considerably relying on your country of house and the certain regards to your IUL policy. In some areas, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, policy loans are normally tax-free, using a significant benefit. In various other jurisdictions, there may be tax effects to think about, such as potential tax obligations on the loan.

Term life insurance coverage just offers a death benefit, without any type of money worth build-up. This indicates there's no cash value to obtain versus. This short article is authored by Carlton Crabbe, Ceo of Resources for Life, an expert in providing indexed global life insurance policy accounts. The details provided in this article is for academic and informative objectives only and ought to not be understood as monetary or investment guidance.

However, for loan police officers, the extensive guidelines enforced by the CFPB can be viewed as cumbersome and restrictive. First, financing policemans often suggest that the CFPB's guidelines produce unnecessary bureaucracy, causing even more documentation and slower loan handling. Rules like the TILA-RESPA Integrated Disclosure (TRID) policy and the Ability-to-Repay (ATR) demands, while focused on securing consumers, can result in hold-ups in shutting offers and enhanced functional costs.

{kind=link}

Table of Contents

Latest Posts

Private Banking Concepts

Become Your Own Bank. Infinite Banking

My Own Bank

More

Latest Posts

Private Banking Concepts

Become Your Own Bank. Infinite Banking

My Own Bank